22nd October 2019

Why do Companies, Chairs (and their Board of Directors) and CEOs fail?

The recent and pending crop of corporate disasters has prompted me to try to answer this question.

The companies themselves and the so-called business media trot out a whole range of superficial excuses about why failure occurred. The current favourite is “Brexit”.

I use two tests of failure:

- Failure on the Stock Market

The Stock Market indicators of failure are that TSR performance is below expectations, and that the share price is falling.

In these circumstances, many Chairmen and CEO’s will claim that the Stock Market is somehow irrational or is biased against their business and that is what is causing the problem.

So, let’s take that excuse away by focussing not on performance on the Stock Market; but on how the business has actually performed in delivering what we call Fundamental Value.

- Failure to deliver Fundamental Value

By this we mean failure to deliver returns higher than the cost of capital that we hope will be translated eventually into increases in the share price

We calculate annual Fundamental Value using the equation:

NOPAT less a charge for all the capital used by the business

(NOPAT = Net Operating Profit After Tax)

We use the book value of equity so the vagaries of the Stock Market are largely removed. Fundamental Value is sometimes referred to as Economic Profit.

So, using Fundamental Value as our measure of performance, the signs of failure are:

- Fundamental Value is in decline – a warning to management

- Fundamental Value is below zero – now we are in real trouble

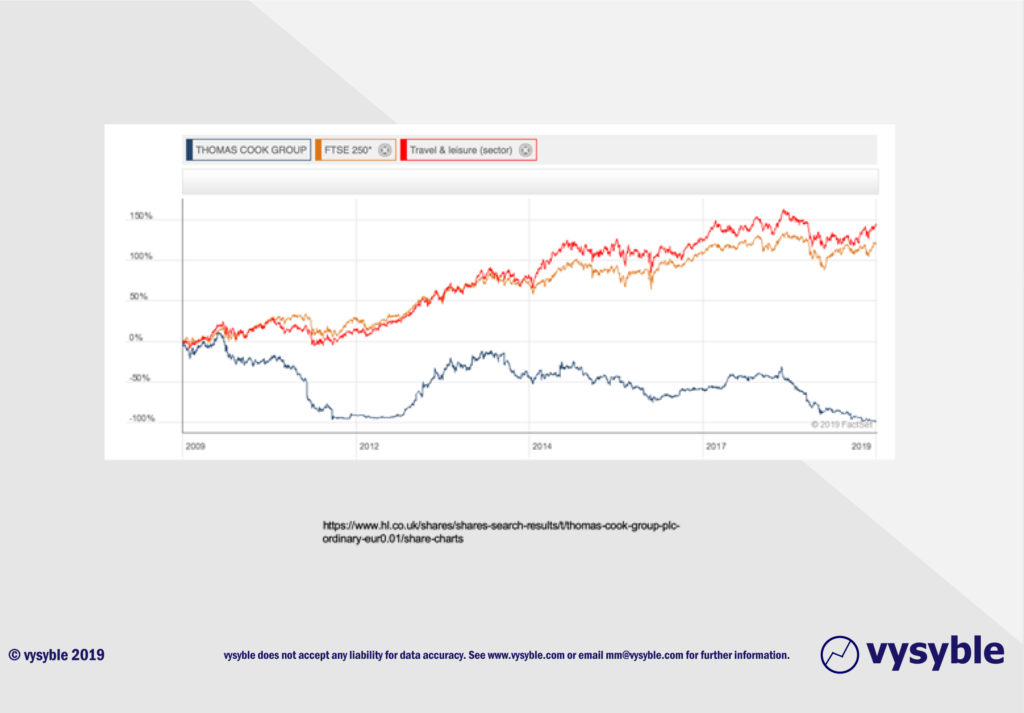

Thomas Cook’s path towards stock market failure is illustrated below:

Here we see Thomas Cook massively underperforming both the FTSE 250 and the Travel & Leisure Sector from 2009. The Board of Directors had plenty of notice that things were not going well….

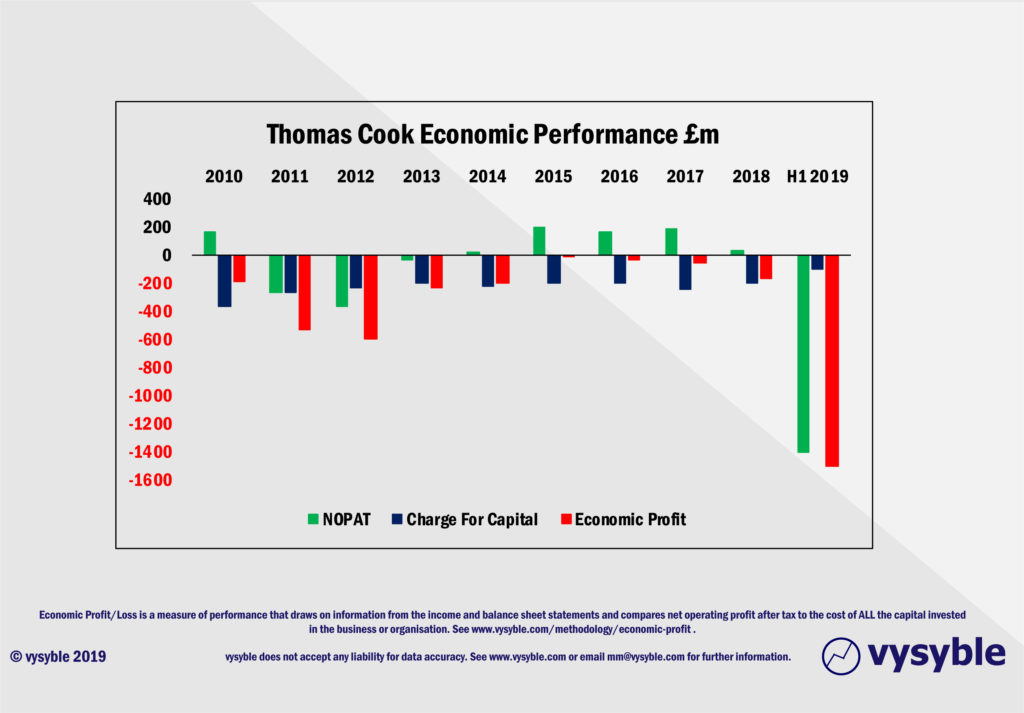

In the above graphic the red bar highlights the company’s Economic Profit performance – it shows that Thomas Cook never once delivered returns higher than the cost of capital. When I see this I inevitably think that the future for the business looks bleak unless something radical can be done.

Once again, we can see the roots of the Thomas Cook debacle as far back as 2010, long before Brexit was on the cards. None of this is new; and it would have been highly apparent to both the Chair and the CEO of Thomas Cook if they had cared to look at the time.

In my opinion and given the evidence presented, the failure of Thomas Cook was rooted in incompetent management and poor standards of governance – a potent and, ultimately, deadly combination.

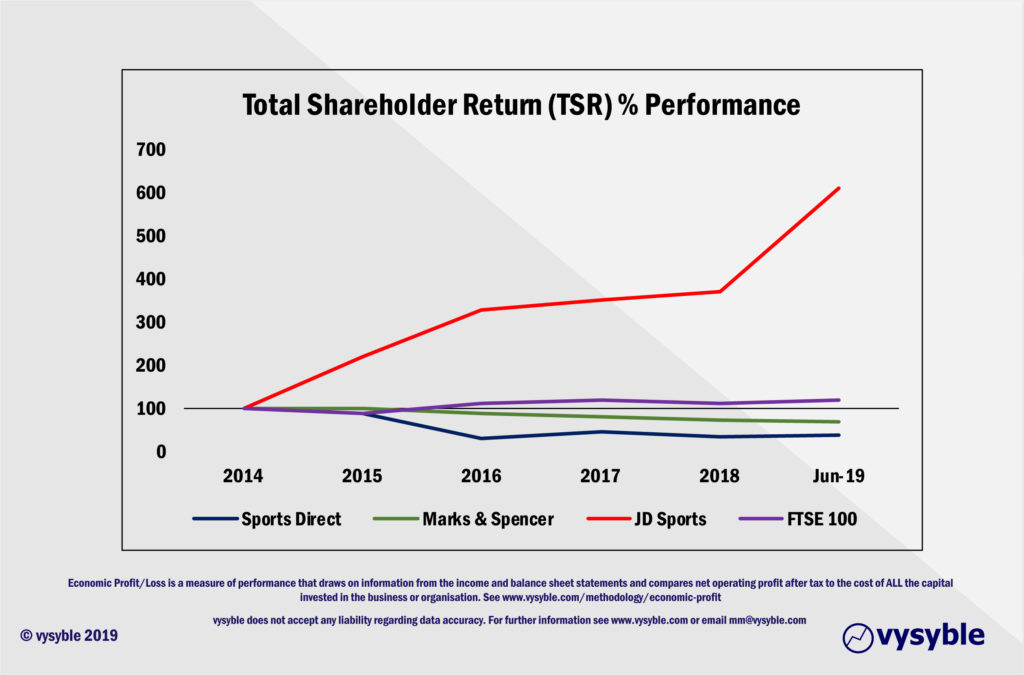

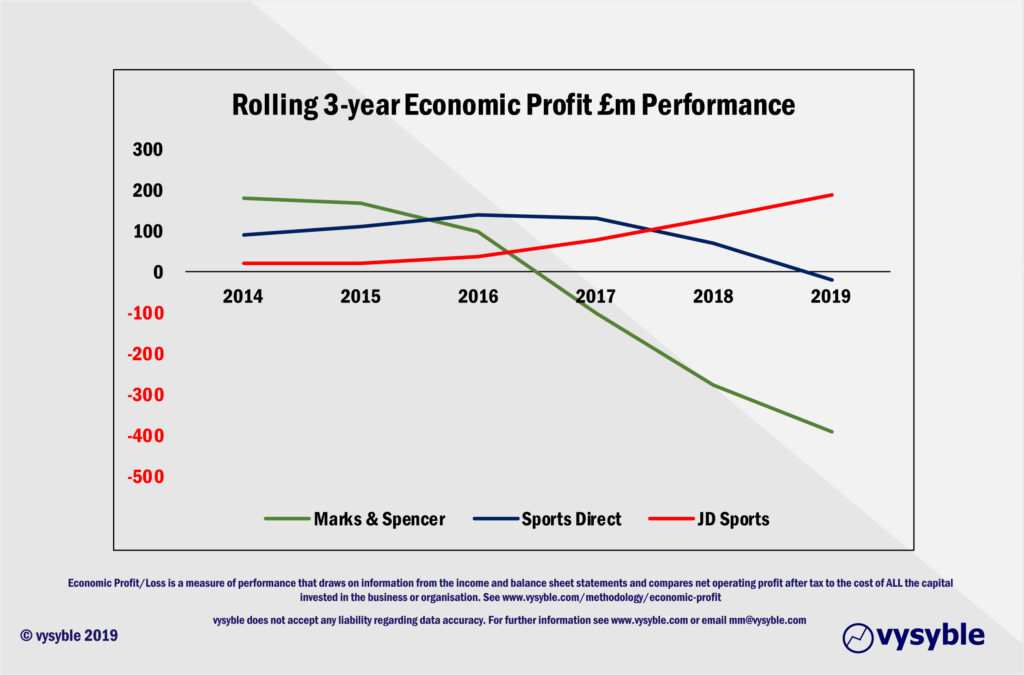

Moving on, two highly visible businesses in most major high streets and shopping centres – Sports Direct and Marks & Spencer – are showing signs of failure – their TSRs are negative and have fallen way behind the FTSE 100. Note how well JD Sports has performed over the same period.

The collapse in the share prices of both M&S and Sports Direct can be explained by the dramatic falls in their delivery of annual Fundamental Value.

Both companies have been – and remain – significant destroyers of Fundamental Value. Their business models do not deliver returns higher than the cost of the capital that is embedded in their businesses. This is an unsustainable situation and bad things lie in store for both businesses if this continues.

What sits at the heart of these and similar failures?

The debate as to why some companies fail meanders through a litany of possible reasons and excuses.

But it seems to me in the highlighted cases that we can pin the blame squarely on the Chairs and the CEOs. Their primary role is to safeguard the future of the business for the benefit of shareholders and stakeholders.

In my experience, the biggest deficiency of current and prospective Chairmen and CEOs is that they lack a robust holistic mental model of their business within its competitive environment. Indeed, they do not know how to ‘think’ about the business.

This holistic framework needs to include some key elements; all critical, none sufficient, and all interconnected. The key components and some common errors are:

- The Stock Market

- Chairmen and CEOs have the wrong ideas about how the Stock Market values businesses and what that means for the business

- They are awash with flawed ideas about how things like EPS and EBITDA are drivers of value

- The Objectives and Aspirations that are set for the business

- The most common error here is to drive the growth of revenue, often at apparently any cost, in the belief that it will always drive value up

- How Strategy is used to drive value

- Strategies end up being wishlists with no basis in the economic realities facing the business in its markets

- How Finance is used to give visibility of value creation and destruction

- Traditional accounting measures are used. These almost wilfully mislead managers about value creation and destruction

- How Organisations can be aligned with value so they can work effectively

- Organisational structures and the ways of working are often not set up to clarify the accountability and responsibility for value. Decision-making becomes confused and slow

- How to give people the skill and will needed to manage value

- People get trained in many things: but not in how to drive the business for value. Incentive schemes often encourage value-destroying priorities and actions

- How to excel at Execution – at getting the right things done to drive value

- Execution can be left to more junior managers – somehow or other, things will get done in a world of ever-shifting priorities

- How to drive and adopt Innovation across the business

- The business finds a myriad of ways to resist change

So the perspective that Chairs and CEOs use to run the business is nothing more than a concoction of disconnected concepts, notions, and received truths that they have picked up and accumulated on the way throughout their careers. Many of these notions are just plain wrong and it is the baggage of inaccuracy which leads them to be ineffective managers of value.

Over the past decades, we have seen the rise of numerous Business Schools and the consequential flood of MBA-qualified people into the global job market. Some have percolated into senior management positions. But in my experience – and I have recruited many MBA-level graduates from the best business schools in Europe and the USA – most are not so well-prepared to take on the responsibilities demanded of a CEO. They are certainly not taught the top-down holistic framework that they need. This needs to change and quickly.

If this is of interest then please contact us using the form situated at the bottom of the home page