25th September 2017

This time around we have a few updates and a couple of observations for you.

Further interest in the application of Economic Profit to football has been kindly provided by Professor Stefan Szymanski from the University of Michigan. Some of you will know Stefan as one of the co-authors of ‘Soccernomics’ as well as a respected authority around the subject of sporting economics. It is on the Soccernomics website that we now have our guest blog entry – ‘Football’s Economic Back-Pass’ – which explains everything you wanted to know about Economic Profit but were afraid to ask by illustrating the economic performance of the English Premier League clubs. We are genuinely delighted and grateful to have been given such a highly-regarded platform other than our own to express our ideas and findings.

If you have been following our Twitter account recently (@seetrends), you will have seen several tweets released for selected games in the English Premier League whereby we give a quick snapshot of the economic position of both teams prior to kick-off. It provides for an interesting talking point and puts the concept of Economic Profit along with other relevant financial measures such as revenue, staff costs and transfer activity directly in front of fans on matchdays. The reaction has been overwhelmingly positive and so we intend to officially launch the service, to be known as ‘Matchday Metrics’, later this week.

We have put the final touches in place to our latest report ‘Over the Line’ which examines the economic costs associated with promotion and relegation into and out of the Premier League. We aim to release the report on 10th October.

The report highlights some fascinating points about the true cost of promotion out of the Championship division as well as the impact of Premier League economic dynamics on promoted clubs and their overall economic performance and vulnerabilities.

Since we published our last blog entry ‘Crystal Balls-Up’ on 12th September 2017 regarding the somewhat questionable Board decisions made at Selhurst Park, another six goals have been shipped without reply. The club’s next game is away to Manchester United followed by a home game with Chelsea. It is entirely conceivable that the club could go 8 games without scoring. We hope that the balance sheet is in good shape as ‘Over the Line’ demonstrates that anything other than prudent fiscal management during a Premier League tenure condemns relegated clubs to a prolonged period in the second tier and sometimes beyond.

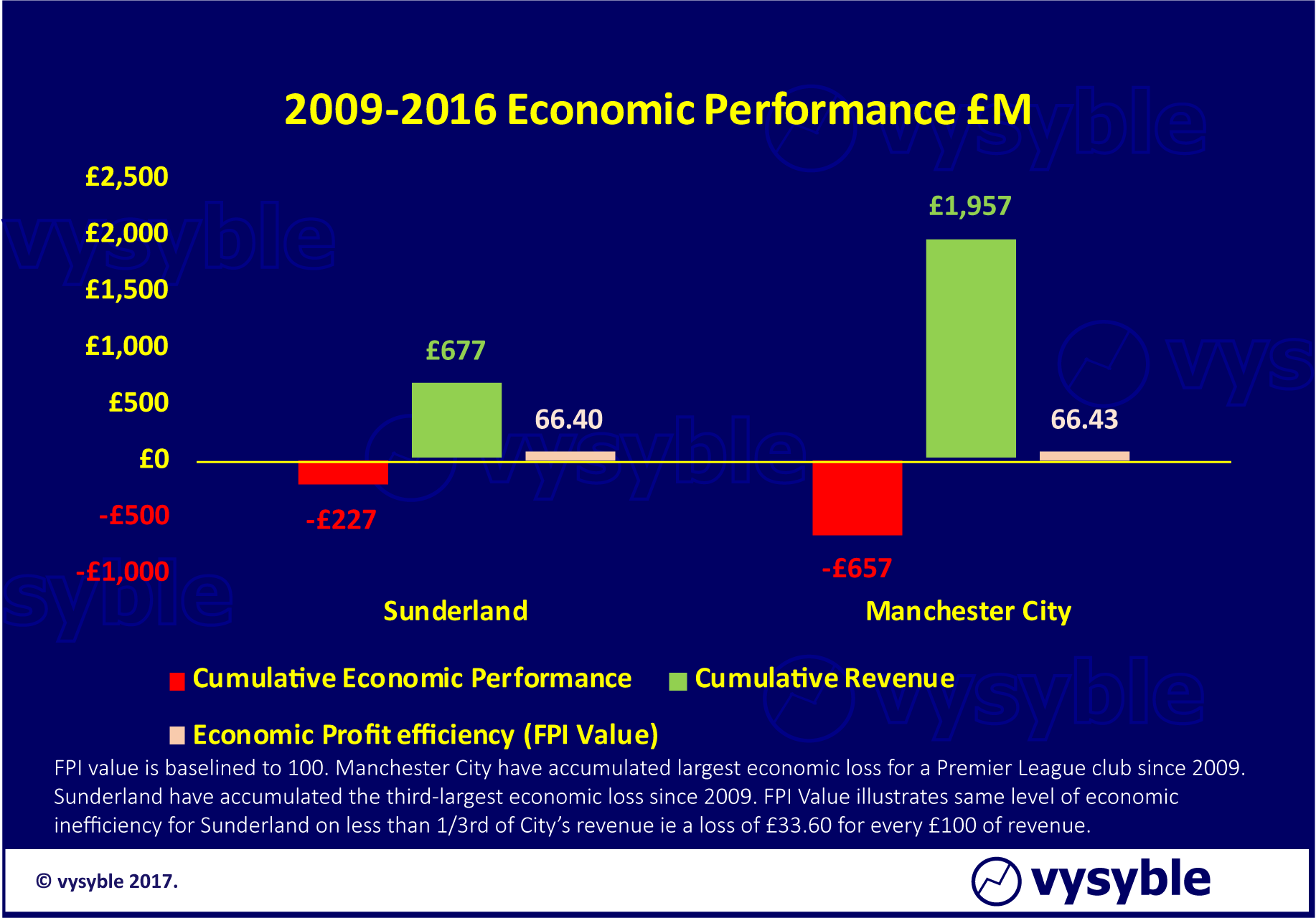

There has been increasing unease within football circles about the overall financial health of Sunderland AFC. Certainly, our calculations show that the club is not in the best of economic positions and will remain so unless there is a significant change in direction and a major capital injection. We have already offered comment about the club’s economic performance in previous reports and blogs and it is a great shame to see such a rich footballing heritage in a difficult spot. If the situation deteriorates further then the club may have to face administration which in turn will entail a probable points deduction.

In our view, the club made the fatal mistake of trying to compete with the big boys on very modest revenues with an underlying and deteriorating economic performance. Sometimes relegation can be beneficial in that it offers a chance to regroup. However, Sunderland appeared to fear relegation so much that it eventually ended up destroying the balance sheet in a long, drawn out and futile survival process. The chart below demonstrates the length to which the club went to preserve its Premier League status in matching Manchester City’s economic inefficiency with much shallower pockets.

The FPI Values are a measure of economic efficiency (see Methodology). To convert the FPI Value into a comparative economic profit or loss per £100 simply subtract 100 from the FPI Value ie Sunderland’s economic loss per £100 of revenue is 66.40 – £100 = -£33.60. This is a large sum to lose over such a long time on what has been a relatively low revenue level by Premier League standards (the same argument could be made of Manchester City despite the larger sums involved but the deeper pockets of its UAE-based ownership ‘sways’ the argument in City’s favour).

Now that the club is indeed relegated, the future looks bleaker than it has for many years whereas if the club had accepted relegation earlier and managed the balance sheet accordingly, there would have been the much better prospect of promotion back into the Premier League and probably sooner rather than later.

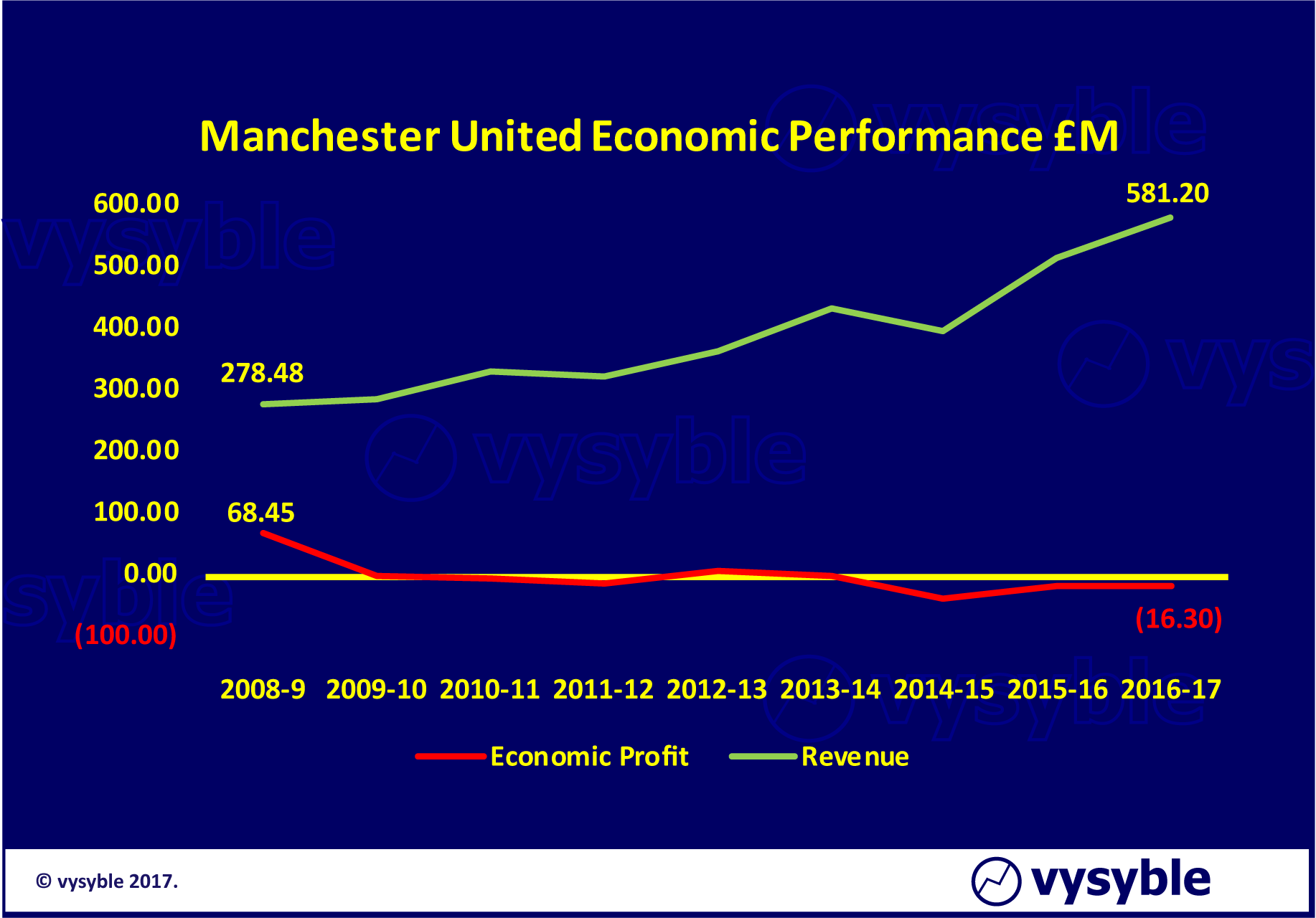

Finally, a comment or two on Manchester United’s full year numbers which were released last week. The revenue rise is impressive and represents one of the largest revenue rises for an English club in many a year. However, the rise in costs, especially in staff, is notable. Thus the club has returned, according to our first set of calculations, an economic loss of £16.3m which is not a disaster by any means. In fact, we view the club as a well-run operation as it does not heavily rely on broadcast revenues (although the share of revenue has increased from 27% to 33%).

What is intriguing, though, is that once again and despite the much-vaunted rise in money into the Premier League clubs due to the £5.1bn domestic TV contract and revenues from additional international media rights, the biggest club in the land did not achieve an economic profit. In our report ‘We’re So Rich..’ we demonstrated that the top 7 clubs by revenue are less-than-consistent when it comes to profit generation. When economic profits do appear, they are usually to be found within the ‘other’ 13 clubs. However, given the inflationary course of the transfer market over the last 2-3 years and the evident inflationary track in player wages, do we dare to even think that the words of optimism touted earlier this year from certain quarters about the future financial health of the Premier League are over-done?

Admittedly, one swallow does not make a summer but we await the other 19 club balance sheets with renewed interest.

vysyble