8th August 2018

Recently there have been several articles and discussions across the media about the prospect of a European Super League. This follows comments back in May from Arsene Wenger. Indeed, our work was quoted and referenced in an article published by Forbes yesterday (7th August 2018) and also used (without reference) by Matthew Syed in The Times today (8th August 2018). We highlighted the Super League topic in our most recent press release of 22nd July 2018.

The European Super League concept has been floated before – we’ve been highlighting this for the last two years as an obvious next-step for football. The recent announcement from Mr Kroenke and his full acquisition of Arsenal has given further emphasis to the increasing influence of American investors to the beautiful game. Again, this is something that we discuss at length in our recently released annual report ‘We’re So Rich…’

Just to be completely clear and in an effort to ensure that our perspective is not accidentally misrepresented, it is worth emphasising that we are fans of the game. From our perspective, we like the fact that Burnley (say) can go to Stamford Bridge and turn Chelsea over. To us this is part of the romantic appeal of sport and we believe that a league without this would be a significantly poorer proposition.

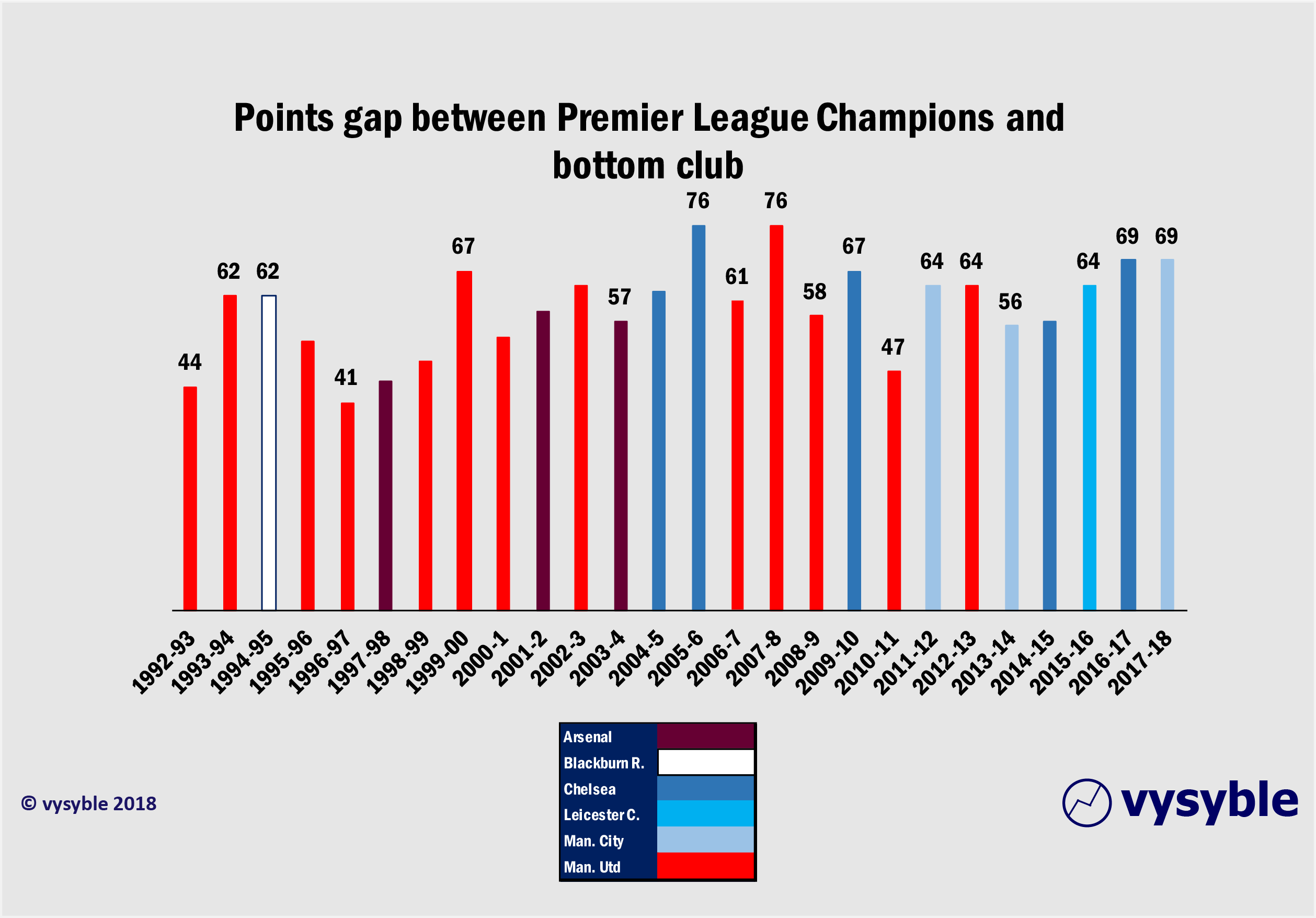

That said, perhaps it is a good idea from time to time to balance our romantic notions regarding the beautiful game with some robust and unfortunately hard facts. Since 1992, only 6 teams have won the English Premier League and 2 of those, Blackburn Rovers and Leicester City have won it on one occasion. In other words, over a 25-year period the EPL has been dominated by 4 clubs – Arsenal, Chelsea, Manchester City and Manchester United.

The entertainment value of the Premier League and the extent of its marketing reach is undeniable but perhaps not as competitive as some would have you believe. In fact, the following chart illustrates that the Premier League is not necessarily a series of random events. The gap between the top and bottom clubs illustrates a near-rhythmic quality and thus strongly suggests that there are underlying and repetitive behaviours at work.

At vysyble, we are concerned about the future of the English game. We do not view a European Super League with unbridled enthusiasm, a position that has been constant since we started to report on football’s fiscal performance. However, when we look at the economic performance of the Top Six clubs together with the negotiating power of the top players and their agents, the reliance on monies from broadcasting plus the increasing influence from across the pond, we think that a change is coming. It is becoming easier to see why it would happen and that is the point that we are striving to make.

Given the scale of Premier League club economic losses (£1.9bn from revenues of £26.1bn between 2009-17) and taking a more conventional “business consultancy” perspective, an equivalent situation in most other industries would trigger change, consolidation and not a little upheaval.

Additionally, we certainly do not think that football has a different economic gravity than other industries or business sectors. After all, the Premier League is populated with businesses that have 9-figure turnovers and are susceptible to all the commercial pressures that any other modern business will encounter. Markets do change and companies have to adapt or face the consequences. The reality is that football is no different.

As part of our media work earlier this week, we were presented with a set of questions to answer as background to a wider article. We have listed them below in full with answers as an insight into our thinking and position on the Super League issue.

A European Super League has been suggested several times before without becoming reality, what’s different now?

The concept of a European Super League has been around for over 40 years. Indeed, the Champions League has been a slow-burn evolutionary process towards a more league-type orientation from the original knock-out format, but it still lacks the certainty and anticipation that a regular club listing and format would deliver.

We think that a super league needs the following elements for it to become a reality;

- a single supportive broadcaster/media distributor that can handle global demand via streaming technology

- increasing indifference by the richer clubs to local competition

- an increasing lack of competition at local level

- consistent economic losses achieved by the top clubs

- business models predicated upon ever increasing TV revenue streams – which in England look like they are going to be static or even falling over the next 5 years.

- a situation where the balance of negotiating power rests with the elite players and their agents – a European “closed shop” league could address this

- a vibrant sponsor marketplace

For the English Premier League (PL) clubs, the end of the 2019-2022 domestic broadcasting agreement is important because we suspect that streaming rights will be a much more critical component than the TV element. In our view, the contractual format and requirements will change which in turn will impact revenue generation as consumption patterns continue to evolve.

In addition, the media landscape is changing. The Comcast/Disney/Fox/Sky situation throws up some interesting scenarios for the PL clubs, especially the Comcast aspect with its ownership of NBC and being the current holder of US rights to Premier League football up to 2022. If Comcast does get to control Sky, then we would expect a CEO-level review in terms of how to maximise value from the separate rights agreements, even to the point of attempting a renegotiation. For the top PL clubs, it may be the catalyst to seek greater and more substantive revenues under a new competition format rather than get involved in a protracted process.

For all its revenue, the top PL clubs (and we suspect the top Italian and Spanish clubs) as a group are also achieving consistent economic losses (PL Big 6 have not achieved economic profit as a group since we started monitoring data in 2009) as they compete amongst themselves for local domination as well as against what has been consistent and superior competition in Europe (from the Spanish clubs in particular). An NFL-type management structure with caps on player costs and a revamped player transfer system would be an attractive proposition for club owners as a way of increasing revenues and reducing costs and which also provides for a more competitive and evenly matched competition. To put it simply, for the clubs there has to be a better way to make a profit.

When we look in more detail at the numbers over time, we can see that most if not all of the Premier League revenue increase (which has been significant) has gone in increased expenses, principally to players and their agents. This is not just an English problem. A properly constructed European League has a chance of achieving a better balance between the interests of the clubs and the players (and their representatives). In other words a European League could, and we stress the word could, address the structural imbalance between the clubs and the players / agents. Our own data indicates that the Premier League has achieved £1.9bn in economic losses on the back of £26.1bn in revenue between 2009-17 thus highlighting this imbalance between club interests and those of the players.

Based on your analysis, how far away do you think a European Super League is (e.g. could it be possible after the next three-year TV deal?)?

PL domestic TV revenues will drop by 9% to £4.654bn based on our estimates for the 2019-2022 cycle. The estimated average rate received per game broadcast will drop 24% from £10.12m to £7.74m partly driven by an increase of 32 games broadcast per season. It is clear that the domestic market is becoming less lucrative for each game played hence the successful play for an increased share of revenues from international media rights by the Big 6 clubs in May 2018.

Given the impending changes in the media landscape, it would be easy to say 2022. Technically, it can be done now. We are aware that UEFA have already run commercial models based on a weekend Super League, so the planning for such an event is already taking place. What is certain is that we are closer to it happening than ever before.

In May, Arsene Wenger suggested a European Super League would be played on the weekends, with the Premier League moved to midweek, whereas in the report you suggest a European Super League would lead to the Premier League’s “ultimate demise”. Why do you think the Premier League would be unsustainable alongside a European Super League? What would the impact be for clubs outside the ‘top six’ of Manchester United, Manchester City, Liverpool, Spurs, Arsenal and Chelsea?

The original premise of the Premier League was to maximise media revenues for the benefit of the clubs. With the top clubs removed from this format, the value to subscribers, sponsors, advertisers and hence broadcasters is very much reduced. We already have evidence of this whereby the EFL Championship (England’s second tier) receives £120m per year from Sky up to 2024 to broadcast games. This is £40m lower than the annual amount paid by Sky to the Premier League back in 1997.

As a result, club finances will deteriorate, and a number of clubs could face the prospect of administration, similar to the collapse of the ITV Digital broadcasting agreement in 2002 when one third of clubs outside of the Premier League ended up in financial difficulty.

Fans may argue that the remnant league will be better off without the top clubs but the financial impact will be significant whatever the quality of football played. It may indeed give rise to a resurgence in home-grown talent as the dual hit from a restrictive Brexit immigration policy and decreased affordability of playing staff reduces the options open to foreign players. However, the commercial flight away from what will no doubt be seen as ‘second-level’ football will, we think, lower quality.

Even if a ‘premier’ league were to run alongside a super league format with certain clubs participating in both, the number and regularity of games would be prohibitive with increased risks to player health. The existence of two leagues is little different from the current situation and offers no improvement on costs or revenue potential due to the lack of exclusivity.

In the interim, we would not be surprised to see an extension of the International Cup competition as a lead-in to a super league format. In turn, we may see certain clubs being more vocal and supportive about playing actual league games abroad as part of a pre-launch strategy.

How significant would the influence of US owners, investors and media interests be in the establishment of a European Super League?

In our latest report we included a quote from James Montague’s book The Billionaire’s Club regarding the NFL’s ability to generate significant profits for franchise owners.

Three of the top 6 clubs by revenue in the Premier League are owned by US individuals and their investment vehicles. All three also own sporting franchises within the US.

The main broadcaster of Premier League games in the UK will be ultimately acquired by a US company once due process has been completed.

Indeed, Wembley Stadium – the home of English football – is in the process of being acquired by the owner of the Jacksonville Jaguars NFL franchise from the Football Association.

The American thread that is increasingly running through the fabric of the English game and into Europe will change the top echelons of European club football into a mirror image of what is familiar and what has been proven to work.

It is clear to us that American thinking has generated significant levels of success for franchise owners across a number of sports ie NFL, NHL, NBA, MLB etc. Unfortunately, the current European football model has hitherto been less successful.

Arguably, the Premier League is a stepping stone towards the European mainland – AC Milan is now under American ownership. Whilst the dynastic mainland European clubs may at this stage be wary of a friendly invader, the rewards for what we see as inevitable change could be considerable under the right economic model. All the chess pieces are being moved into position.

We believe it is only a matter of time.

vysyble