30th March 2021

Previously, we have written and discussed the similarities and differences between Arsenal and Manchester United from a balance sheet and financial performance perspective as part of a wider analysis of the North London club’s overall business position.

The latest set of financial results from the 2019-20 season prompts a revisit given the unusual circumstances that unfolded towards the season’s end which in itself was extended into the summer months.

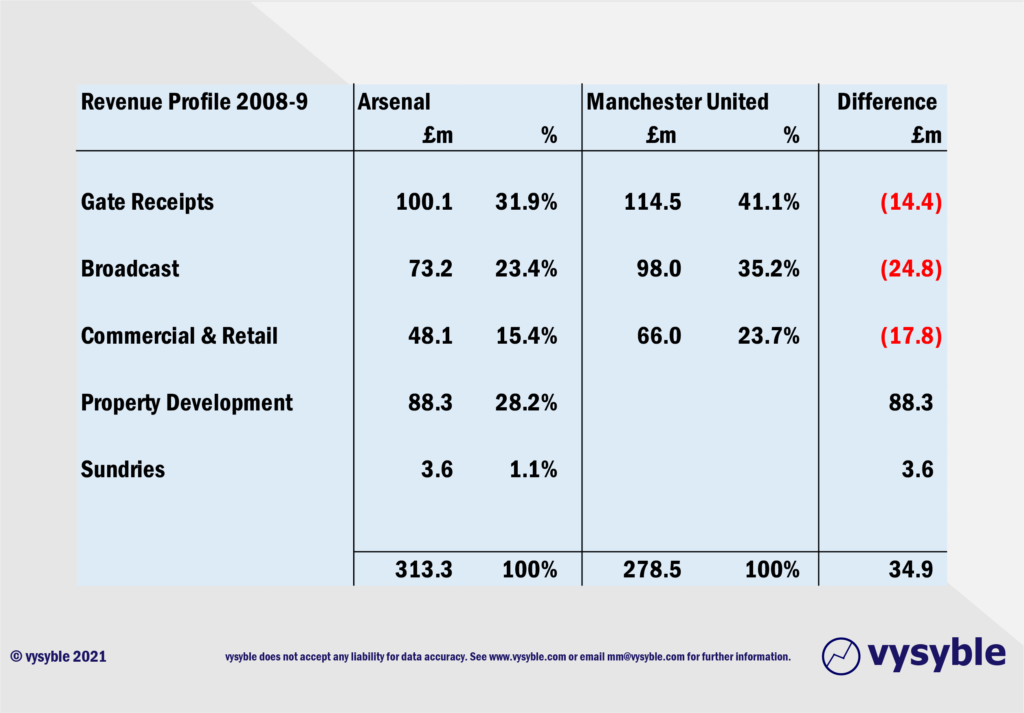

So, to start off, we will indulge in some time travel all the way back to the angst of 2009 when the world was still reeling from the banking crisis of the previous year, the death of Michael Jackson and Manchester United winning yet another Premier League title with a total of 90 pts, ahead of Liverpool in second place on 86 pts and Arsenal in fourth place with 72 pts.

From a revenue perspective, both Arsenal and Manchester United where broadly similar…

Largely due to revenues from property development offset by lower receipts from gate receipts, broadcasting and commercial activities, Arsenal’s turnover came in at £34.9m ahead of Manchester United.

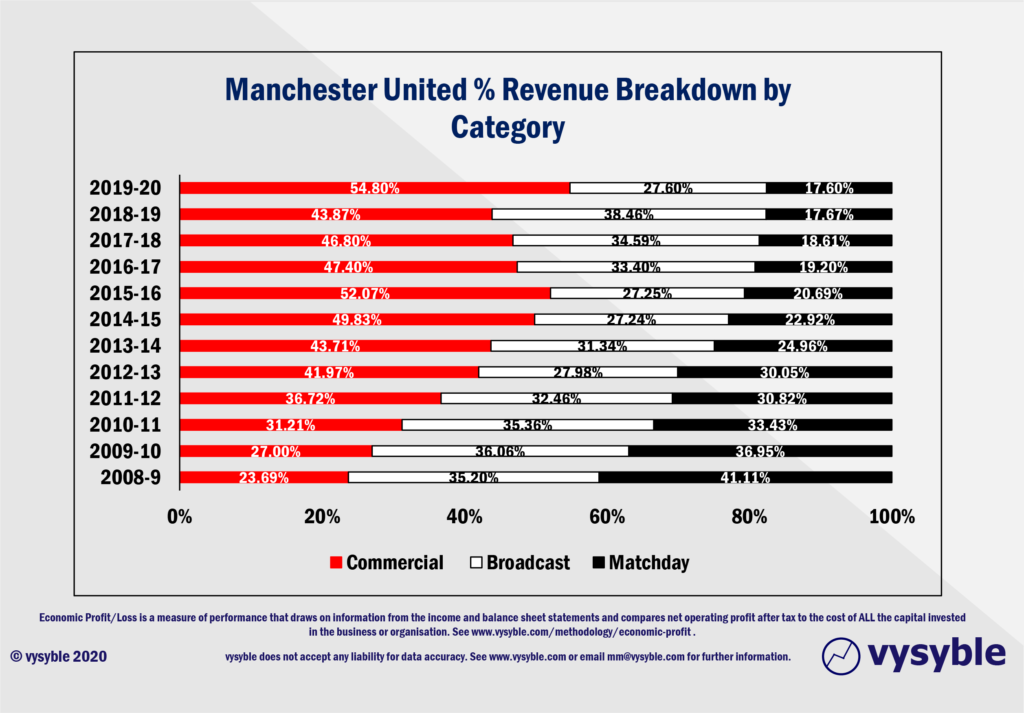

It is interesting that for both clubs the largest driver of revenue back in 2009 was gate receipts which accounted for 31.9% and 41.1% of Arsenal’s and Manchester United respective revenue totals. When viewed through this lens, a larger and more modern stadium was understandably seen as a positive and potential route to financial outperformance despite the requirement of significantly more capital on the balance sheet.

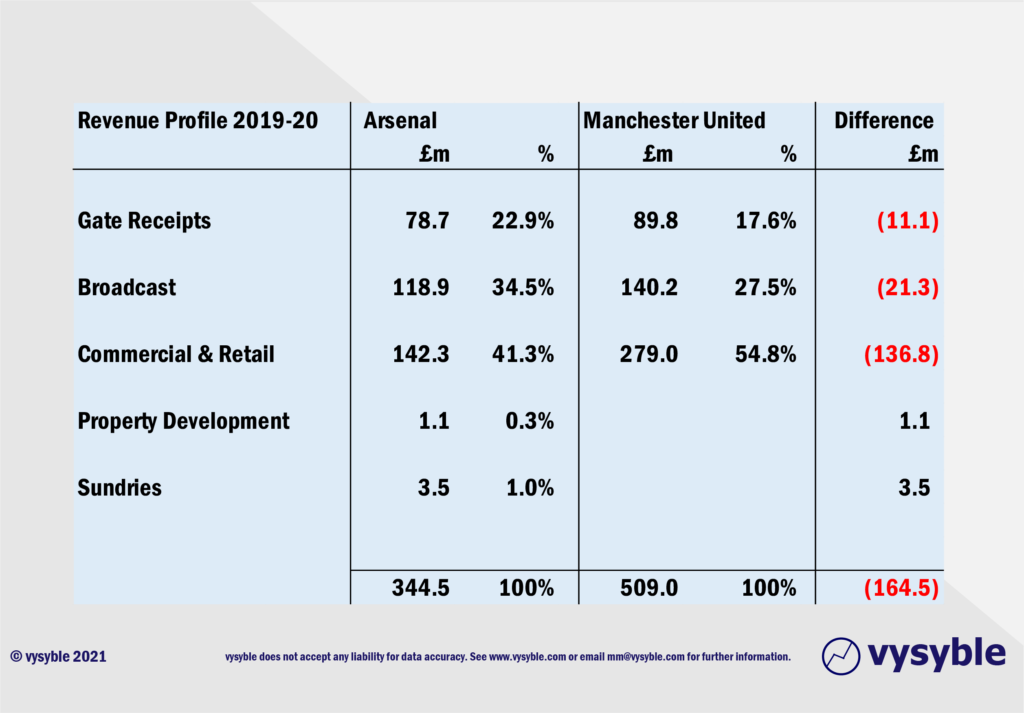

Moving swiftly into 2019-20, we find both clubs in quite different positions from a revenue perspective…

Covid-19 has obviously affected both clubs with a number of fixtures taking place in empty stadiums. Gate receipts have indeed been hit but that said, in the eleven years since 2009, Arsenal’s revenue has grown from £313.3m to £344.5m per annum – an upward movement of just £31.2m or 9.96% uplift.

Indeed, the North London club’s gate receipts in 2009 totalled £100.1m. However, gate receipts had dropped to £78.7m in 2019-20, some £21.4m lower than the 2009 level. The beginnings of football under Covid-19 had already made its mark.

By contrast, Manchester United’s revenue has grown from £287.5m (2009) to £509.0m (2019-20). This is an increase of 80.1% (£230.5m) or in comparative terms, approximately 8x Arsenal’s own revenue uplift for the same period. Like Arsenal, Manchester United’s gate receipts in 2019-20 were £24.7m lower than the 2009 total of £114.5m.

The largest component of revenue for both clubs in 2019-20 was not gate receipts but the commercial and retail element. Manchester United’s prowess in generating commercial revenues over the last decade or so has been covered many times across numerous media outlets. Nevertheless, the comparative performance with Arsenal demonstrates how one club got it right and one club got it wrong.

In 2019-20, Arsenal generated £142.3m in commercial revenues. Manchester United achieved a commercial revenue of £279.0m which is the largest total for any football club in the United Kingdom.

It therefore follows that the growth or the change in commercial income for Manchester United is the largest driver of the revenue differential between the two clubs.

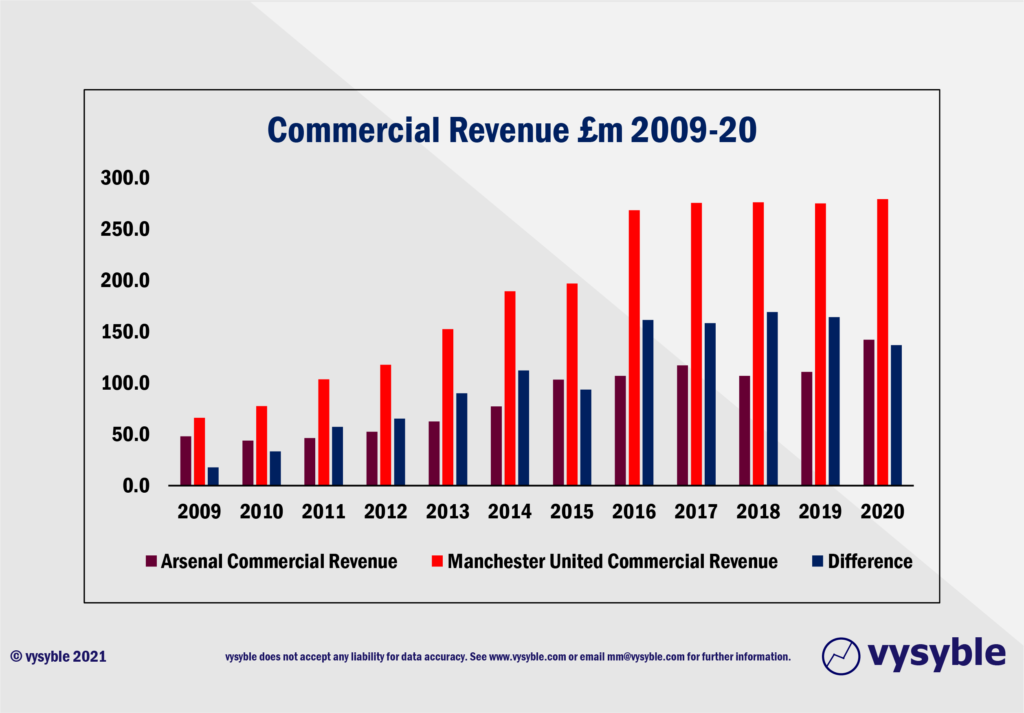

Set out below is a graphic showing the commercial income performance of both clubs since 2009;

So What?

We have consistently stressed that the error of conflating revenue with value creation lies at the heart of many of the misunderstandings regarding the financial and economic health of the beautiful game; a failure to recognise performance based on an actual value creation metric being the most notable.

Indeed, although Manchester United’s ability to generate revenue growth is undoubtedly impressive, it is not, based on the available evidence and in our opinion, a share to invest in for the retirement plan. There are plenty of opportunities elsewhere to obtain a significantly higher return for less ‘risk’.

However, with all of that acknowledged, there are some interesting insights coming from the above graphic.

Over the period 2009-20, Manchester United generated £2.28bn in commercial revenues vs Arsenal’s £1.02bn. The gap between Manchester United’s and Arsenal’s commercial revenue over the 2009-20 time period amounts to £1.26bn. This is £240k larger than Arsenal’s overall commercial revenue of £1.02bn for the same period. A staggering result.

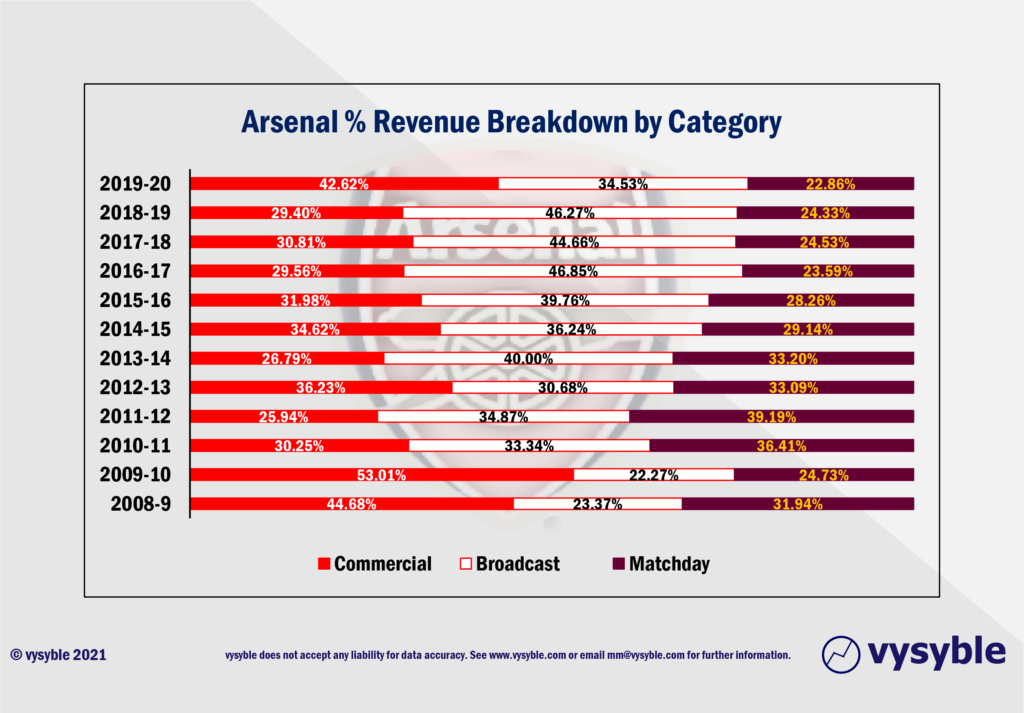

Indeed, when the commercial performance of both clubs are directly compared as a percentage of overall revenue, the strategic element in Manchester United’s revenue evolution from 2009 is absolutely clear vs the haphazard and listless approach seemingly adopted by Arsenal over the same period, as illustrated below;

For comparison, over the period 2009-20, Manchester United’s commercial income grew at 14% per annum compound against Arsenal’s rate of 10.4% per annum.

In 2018-19, the last reported year when gate receipts remained unaffected by the pandemic, Arsenal reported a matchday income total of £96.24m. In 2019-20, the gap between Manchester United’s and Arsenal’s commercial income totalled £136.8m. Take a moment for that to sink in. The gap in commercial performance between the two clubs is bigger than Arsenal’s matchday revenue.

Despite revenue growth that many companies can only dream of, Manchester United have struggled to translate that revenue into economic returns or surpluses. However, there is no denying that the club’s growth in commercial revenue performance is impressive and enables the club to compete for talent that is probably beyond the reach of Arsenal.

With this in mind, we have long believed and stated that the most important executive appointment within Arsenal FC after the first team manager is the marketing/commercial director and the latest data has not changed our view.

It is evident that the commercial potential of the club has not been fully exploited and the continuing failure in this regard is already impeding activity in the transfer market and progress on the pitch. And with imminent change in the structural make-up of football at the highest levels, Arsenal will fall further behind unless it addresses this performance deficit.

vysyble

Follow vysyble on Twitter

22nd February 2021 – Measure for Measure – Take two financial measures, add pandemic and stir.

18th January 2021 – The Football Factory – If football was an industrial entity…

8th January 2021 – The Oil Majors – An Update – A shareholder return performance review of the 4 major oil companies in 2020.

10th December 2020 – Pump Up The Volume – ExxonMobil comes under fire from an agitated investor.

16th November 2020 – The Pain Game – Manchester United’s Q1 2021 financial release opens the lid on a Covid-19-affected financial can of worms.

11th November 2020 – A Tight Squeeze – Football’s Elephant in the Room leaving little space for financial relief.

29th October 2020 – Form and Function – Proposals-a-plenty for football’s structural reform.

13th October 2020 – Project Big Profit – Americans come bearing a proposal for football’s structural reform, just as we predicted in 2016.

8th October 2020 – Game Aid – Football is caught in the crossfire of indecision and financial necessity.

24th September 2020 – Crisis? What Crisis? – We look back 12 months at the demise of Thomas Cook and its relevance to more recent events.

11th September 2020 – Distance Learning – New rules and new values as Covid-19 challenges traditional mindsets and misconceptions.

19th August 2020 – Socked! Marks & Spencer’s Shrinking Value – Retail giant is fast becoming a shadow of its former self.

22nd May 2020 – You’re Gonna Need a Bigger Boat – An assessment of the double financial whammy of potential relegation from the Premier League and Covid-19.

30th April 2020 – Home, Alone – Initial indicators from the wider economy point towards economic and financial downsizing in sport.

6th April 2020 – Board Games – Government, football clubs and players adopt separate ‘brace’ positions as Covid-19 crashes the sports economy.

27th March 2020 – Markets, Mayhem and Manchester United – A look at the questions posed by the share prices of publicly listed businesses.

15th March 2020 – When Saturday Goes – Football has come to a halt. We take stock of the game’s position and ponder its return.

10th March 2020 – Futureworld – The potential economic effects of the COVID-19 outbreak.

19th February 2020 – Lemon Law – How Financial Fair Play can give a misleading view of football club finances.

8th February 2020 – Hammered – Our financial perspective on some of the clubs involved in the Premier League relegation battle.

12th December 2019 – The Cost of Chasing Gold– In collaboration with the BBC, we look at the high price being paid by clubs to gain promotion into the Premier League.

7th November 2019 – Where to Next for M&S? – November 2019 results suggests the retailer is losing its way

10th October 2019 – Red Mist – Manchester United’s 2019 FY numbers and the stagnation of England’s biggest revenue-earning club.

7th September 2019 – Not Just A Loss But… – A detailed look at the decline in Marks & Spencer’s fortunes.

29th August 2019 – Telling It Like It Is… – What really happened when we talked to the English Football League.

5th July 2019 – Chopping Board – Knives out for former Tesco chief.

25th May 2019 –Repeat Prescription – Few believed us the first time around regarding football’s financial plight…

19th March 2019 – Stuff and ‘Nonsense’– Why the Economic Profit metric is the most transparent measure of business performance.

13th March 2019 – Financial Fair Play – Guilty as Charged? – Our thoughts on FFP schemes and their key weakness.

18th December 2018 – Long Division – The Post-Ferguson years at Old Trafford have come at the expense of declining economic and on-pitch performance.

20th November 2018 – The Relegation Game – Tales of woe and economic performance at the wrong end of the Premier League table.

9th October 2018 – A Different View – Why fans ought to be acutely aware of football’s financial dynamics.

17th August 2018 – The End of the Beginning – La Liga heads west to conquer new worlds.

9th August 2018 – Reaching for Sky – the sequel – Latest offer price for satellite TV company is good for shareholders, less so for prospective owners.

8th August 2018 – American Dreams – English Premier League economic dynamics and American money – is a Euro Super League the next step?

3rd August 2018 – Mall Administration – Retail Property Co. bonus payouts at odds with increasing shareholder value.

20th April 2018 – Goonernomics Part Deux – The departure of Arsene Wenger…

18th April 2018 – The Price of Everything – Tesco’s latest numbers offer little in value.

12th April 2018 – Say What? – WPP’s very mixed message.

14th February 2018 – In Case of Emergency – Premier League’s UK TV rights auction comes up short.

7th February 2018 – Lost in Transmission – Top Premier League clubs look beyond domestic TV rights.

4th December 2017 – A Billion here, a Billion there… – The Premier League reaches a major milestone, quietly…

25th November 2017 – Getting out of Toon. – Is Mike Ashley pitching the sale price of Newcastle United at the right level?

16th October 2017 – Goonernomics. How the ‘Bank of England’ club falls short of its North London neighbour.

25th September 2017 – Highlights. More record-breaking numbers from the biggest football club in the land, but no economic profit…

23rd September 2017 – Football’s Economic Back Pass. A guest blog for the Soccernomics website.

12th September 2017 – Crystal Balls-up. Changing strategic direction is not a good idea when you haven’t looked at the economics.

27th July 2017 – Football’s Summer of Money and the £65 pint of beer. The sport that just can’t spend enough.

11th July 2017 – Football Special. Observations following the launch of ‘We’re So Rich…’

9th May 2017 – Illuminating, non? Political energy lacks vision and power.

2nd March 2017 – Claudio’s Burden. The price of failure outweighs the price of success.

12th January 2017 – Shopping for Godot. A never-ending quest for value in Retail.

27th December 2016 – Reaching for Sky. Is Rupert Murdoch’s £10.75 per share a fair price?

6th December 2016 – Auld Lang Syne. A reminder from history of the damage that poor financial planning can cause.

1st December 2016 – Fork Handles? Four Candles? Tesco’s blurred strategic vision.

27th November 2016 – Football’s Instant Replay. Financial warning signals for the top English Premier League clubs.